A new government-backed savings account called Trump Accounts, is launching in July 2026. On the surface, it sounds like a win. Free money for newborns, a long-term investment plan and a head start in creating real wealth. Trump accounts, however, do raise questions about taxes, flexibility and whether they beat existing options such as 529 plans or custodial accounts. Let’s look at the big picture and examine the pros and cons.

A new government-backed savings account called Trump Accounts, is launching in July 2026. On the surface, it sounds like a win. Free money for newborns, a long-term investment plan and a head start in creating real wealth. Trump accounts, however, do raise questions about taxes, flexibility and whether they beat existing options such as 529 plans or custodial accounts. Let’s look at the big picture and examine the pros and cons.

Big Picture – Anyone with a child age 18 or younger who is a US citizen with a Social Security number can open a Trump account. The federal government will contribute $1,000 in seed money per account for kids born between 2025 to 2028. The child owns the account with the parent as custodian until age 18. Others can contribute up to $5,000 per year (adjusted for inflation). Employers can contribute up to $2,500 per year (this counts toward the $5,000 annual cap). Monies can only be invested in low-cost US equity index funds. Withdrawals are taxed as ordinary income and early withdrawals may incur penalties.

Advantages – The $1,000 government seed is hard to ignore, and investing at birth gives compounding 18 years to work. Automatic investing removes decision paralysis and with fees capped well below industry averages, the account can grow meaningfully.

Advantages – The $1,000 government seed is hard to ignore, and investing at birth gives compounding 18 years to work. Automatic investing removes decision paralysis and with fees capped well below industry averages, the account can grow meaningfully.

Criticisms – Parents (or other contributors) must be aware that withdrawals are not allowed for any reason for years before the child turns 18. Contributions will require filing an annual gift tax return. Beginning in the year the child turns 18, Trump accounts automatically assume the normal traditional IRA rules and a 10% early withdrawal penalty will apply to a taxable distribution taken prior to age 59 1⁄2, unless an exception exists.

Observation – Trump accounts do not have the same tax advantages as 529 accounts, which are deferred savings plans designed to help pay for educational expenses. At age 18 or older, if the goal is not to maintain the Trump account as a retirement vehicle, then an UTMA/UGMA custodial account would make more sense. Funding a Trump account might be wise if the intent is to maintain the account as a retirement vehicle.

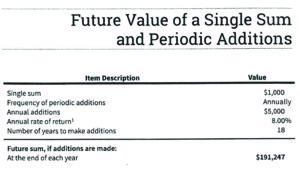

Do the Math -$1,000 in government funds, $5,000 contributed each year for 18 years, 8% annual compounded rate of return $191,247 future sum. With the child now age 18, let’s convert this traditional IRA into a Roth IRA. Assume for the sake of simple math a tax liability of $41,247 leaving a Roth IRA balance of $150,000. The “rule of 72” says that money will double every 9 years with an 8% annual compounded rate of return. At age 27, the Roth is now worth $300,000, at age 36 / $600,000, at age 45 / $1,200,000, at age 54 / $2,400,000, at age 63 / $4,800,000.

Eighteen years of steady contributions from parents, grandparents and employers, a timely Roth conversion with forty-five years of compounded growth – who wants to be a millionaire?

Financial Planning and Advisory Services are offered through Prosperity Capital Advisors (“PCA”), an SEC-registered investment advisor. Registration as an investment advisor does not imply a certain level of skill or training. PCA does not provide tax or legal advice.